- May 19, 2022

- Posted by: BCCI-Editor-M

- Category: Blog

BUSINESS PERSPECTIVE

The Trade License Regime: A ‘tax’ by any other name

“The mere fact that something is labelled a ‘fee for services’ does not necessarily preclude it from being a tax. In other words, an imposition that must be paid, whether or not the relevant services are acquired and that has no discernible relationship to the value of the services, is unlikely to escape characterisation as a tax. … The High Court held that for a ‘charge’ to be considered a ‘fee for services’, it must be ‘exacted for particular identified services provided or rendered individually to, or at the request or direction of, the particular person required to make the payment”—Justice Michelle Gordon (2012).

The opening quote from Justice Gordon, writing in the Melboure University Law Review, draws a distinction between a “fee” and a “tax.” Gordon articulated a commonly held position among legal and financial minds: That a fee is charge “exacted for particular identified services provided or rendered individually to…the particular person required to make the payment.” There is a type of proportionality inherent in a “fee”—That is, you get exactly what you pay for.

A tax, on the other hand, is viewed more generally and for general-revenue purposes. Gordon (2012) phrases it this way: “An imposition that must be paid, whether or not the relevant services are acquired and that has no discernible relationship to the value of the services, is unlikely to escape characterisation as a tax.”

Put simply, the weaker the linkage between the “charge” (regardless if is nominally called a ‘fee’) and the services rendered, the more likely it is we are dealing with a tax by design. This is especially true when the imposition is clearly for general-revenue purposes.

General Revenue Purposes

It is no secret that the Trade License Regime—a vestige of our colonial past—has become a significant (albeit disconcerting) source of “revenue” for

the nine municipalities; namely, Belize City, Belmopan, Dangriga, Punta Gorda, San Pedro, Corozal Town, Orange Walk Town, San Ignacio/Santa Elena, and Benque Viejo.

the nine municipalities; namely, Belize City, Belmopan, Dangriga, Punta Gorda, San Pedro, Corozal Town, Orange Walk Town, San Ignacio/Santa Elena, and Benque Viejo.

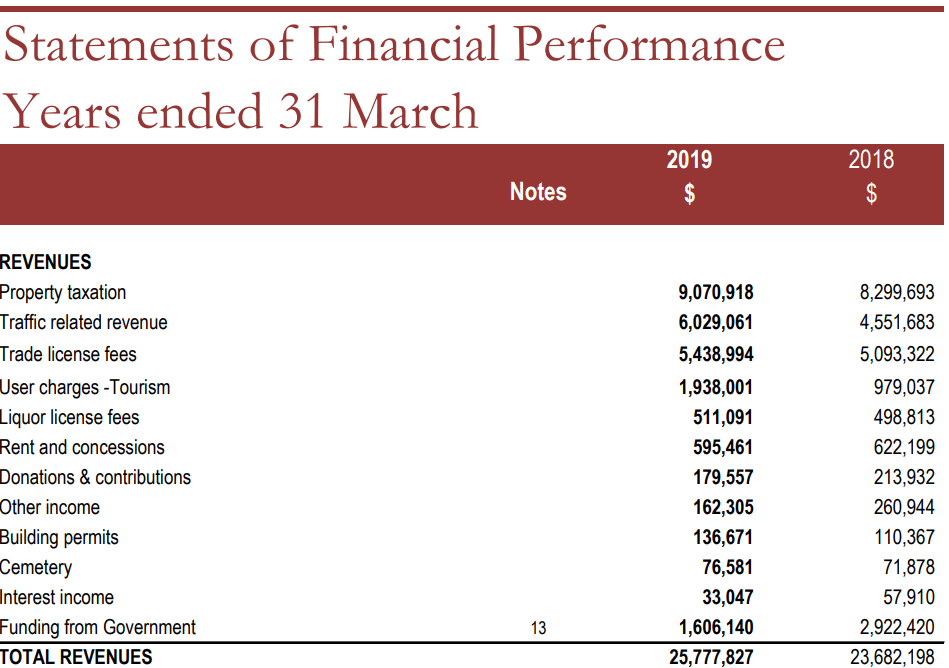

For example, in Belize City, the Trade License “fee” (“TL fee”) generated $4.3 million, a figure that accounts for roughly 18% of the council’s total recurrent revenues (Belize Council’s Financial Report, 2020). A year early—in pre-COVID times—CitCo’s audited financials for 2019 placed the “fee” at $5.4 million, which represented 21% of the council’s total recurrent revenue for that year.

It might surprise a few, but the TL fee far outstrips even the contribution from liquor licensing fees (plural given the different types of liquor licenses). In 2019, CitCo’s financials informs that liquor licenses generated just above $500,000, or only about 2% of total recurrent revenue. That is, however, to be expected considering how and on whom the Trade Licensing regime is applied.

Under the current law, the TL fee is charged as a percent (25% by law) of a business’s annual (rental) value (ARV). Consequently, if a business has an ARV of $30,000, the strict application of the Trade Licensing Act—as it currently stands—would imply a “fee” of $7500. For a business with an ARV of $50,000 the charge would be $12,500.

Property-Tax by Design

Now, you may be sitting there reading this article and asking yourself: “But doesn’t a charge based on annual rental value sound awfully similar to a property-tax valuation methodology?” The short answer to your question would be a resounding “Yes!” Look up “Annual Rental Value” online and you are likely to find statements like this one:

“Annual rental value based property tax systems tend to be originally based on the British rating system and are most commonly found in the former British colonies.”

At this point, you may ask another naturally following question: “But wait! Don’t the municipalities already have revenues flowing from property taxes?” At this point, you’d be on a roll, because you would be right, yet again! Keeping with the Belize City Council’s financials, the 2019 report shows that property taxation provided close to $9.1 million (or 35% of CitCo’s total revenues). This property tax, however, is based on Market Value (i.e. how much the property could be sold for) as opposed to ARV (how much it could reasonably be rented for).

International Best Practices for Fees

Having briefly summarized that status quo, it becomes useful to outline a few of the international best practices as far as “fees” are concerned.

First, international best practices have repeatedly advised that licensing fees—if we accept that any should be instituted at all—should be only sufficient to cover administrative costs. More precisely, benchmark calls for such charges to be flat fees, and thus, ought not to serve as a means of generating revenues for (local) government.

Second, business activity produces net-positive social benefits, and as such ought not to be subjected to a duty just in order “to establish and operate.” The duty or fee, therefore, should be for a legitimate public-interest purpose such as public safety and health. For this reason, one could comprehend the role of liquor licensing regime.

It is worth noting that the liquor licensing regime, as instituted under the Intoxicating Liquor Licensing Act’s section 3, actually operates more appropriately as an actual fee system. For instance, the law sets a fee of $750 for the “restaurant (liquor) license” for any restaurant operating in urban areas. If you are a restaurant with a single bar—regardless of the size of the physical location—the fee (under the Act) is set. For a nightclub, the liquor license is $3,000. Both examples are more consistent with international best practice.

That said, here’s an intriguing side-bar observation. In many instances, the flat-fee design of the liquor licensing regime makes obtaining a license to sell alcohol cheaper than the license to simply start at business. In Belize City, for instance, the average for the TL fee is about $1,900, and it ranges from as low as $25 to as high as more than $100,000. There are close to 300 companies in Belize City that pay a TL “fee” of more than $3,000—that is, more than the nightclub (liquor) license fee.

That “side bar” observation (pun intended) raises some interesting policy questions. Alcohol is largely recognized for its harmful societal impacts. On the other hand, non-liquor-related business activity (e.g. Business Processing Outsourcing centers, law firms, convenience stores, gyms, food vendors, bakeries, and so on) are SUPPOSEDLY welcome additions to communities. If the latter is true, then one—from a public-policy vantage point—would have to rationalize and justify how it is possible have TL fees higher than a nightclub (liquor) license, for instance. This inadvertently sends mixed signals. Or better yet, it inadvertently sends the wrong signal: That non-alcohol-oriented business activity is less desired than liquor sales.

Conclusion

In this Business Perspective Column, we opted to layout the general backdrop for this ongoing Trade Licensing discussion. In the second part of this piece which will be published next week, we will—with this background in mind—lay out the Belize Chamber of Commerce and Industry’s position as it pertains to the proposed amendments to the regime.

")

")

- Header")